BUDDHIST DISCLOSURE ETHICS: BUDDHIST INSTITUTIONAL CAPITAL AS A DETERMINANT OF ESG REPORTING QUALITY

Keywords:

ESG Reporting Quality, Buddhist Disclosure Ethics, Buddhist Institutional Capital, Asian Context, Informal InstitutionAbstract

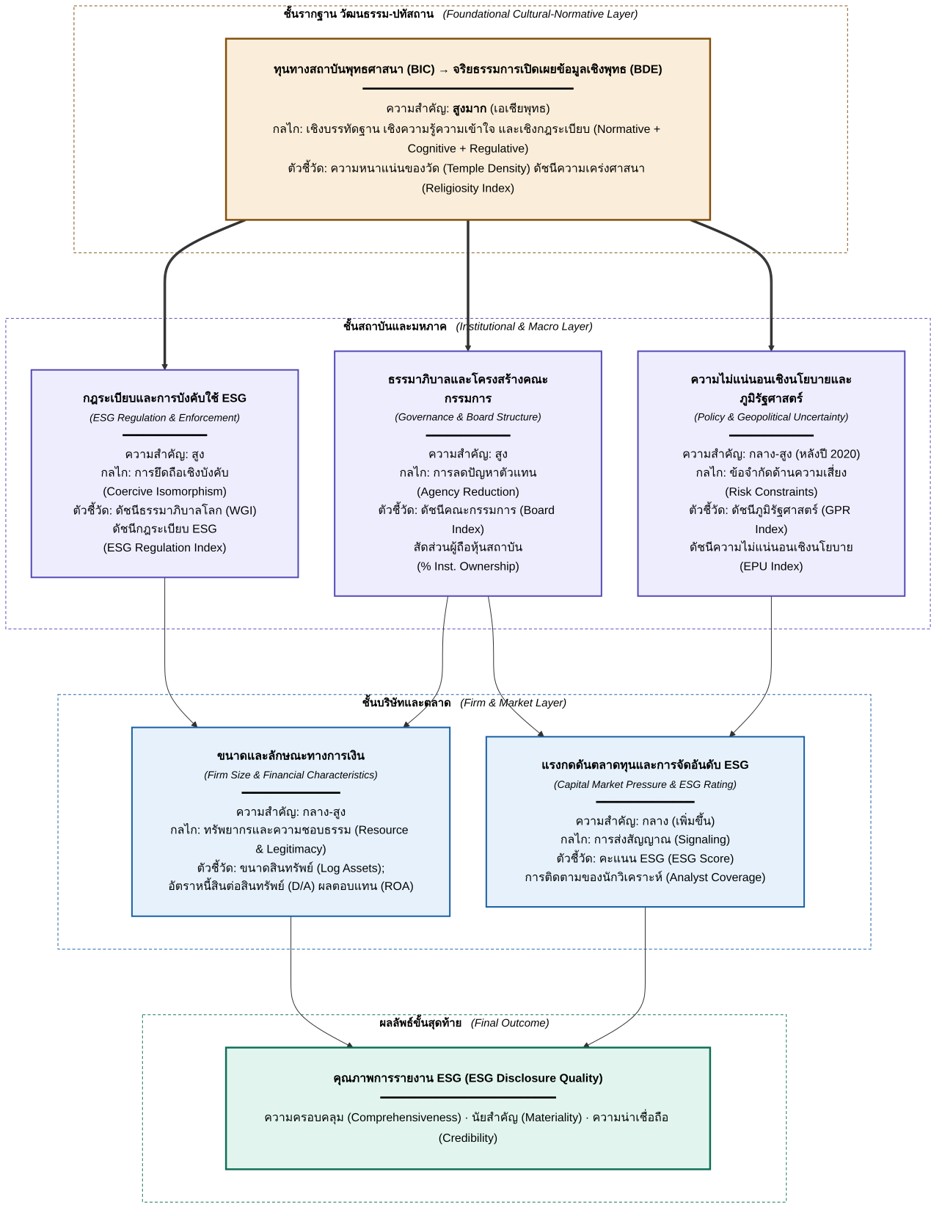

This academic article develops a novel conceptual framework termed "Buddhist Disclosure Ethics" (BDE), which explains the mechanisms through which Buddhist Institutional Capital (BIC) transmits to ESG (Environmental, Social, and Governance) reporting quality in the Asian context, drawing on evidence from multiple regions, structured around four thematic issues. First, with respect to the BDE framework, five Buddhist principles Right Speech, Dependent Origination, Right Livelihood, Loving Kindness and Compassion, and Impermanence and Non-self generate intrinsic motivation for ESG reporting that is qualitatively distinct from compliance-driven reporting, operating through three disclosure quality dimensions: breadth, materiality quality, and substance. Second, with respect to BIC-to-BDE mechanisms, BIC operates through three institutional channels normative, cognitive, and regulative with empirical support at both organisational and regional levels. Third, with respect to ESG reporting quality determinants from the international literature, BDE complements and is theoretically distinct from existing internal and external determinants, because it operates at the value level prior to regulatory and market incentives. Fourth, with respect to ESG rating divergence, BDE proposes an institutional solution by building intrinsic reporting motivation that reduces the gap between symbolic and substantive ESG disclosure. The article concludes with policy implications for ASEAN regulators and directions for empirical research.

References

พระธรรมปิฎก (ป.อ. ปยุตฺโต). (2562). พุทธธรรม ฉบับปรับขยาย. (พิมพ์ครั้งที่ 55). กรุงเทพมหานคร: มหาจุฬาลงกรณราชวิทยาลัย.

มหาจุฬาลงกรณราชวิทยาลัย. (2539). พระไตรปิฎกภาษาไทย ฉบับมหาจุฬาลงกรณราชวิทยาลัย. กรุงเทพมหานคร: โรงพิมพ์มหาจุฬาลงกรณราชวิทยาลัย.

Abeydeera, S., Kearins, K., & Tregidga, H. (2016). Buddhism, Sustainability and Organizational Practices: Fertile Ground? Journal of Corporate Citizenship, 61, 44–70.

Avramov, D., Cheng, S., Lioui, A., & Tarelli, A. (2022). Sustainable investing with ESG rating uncertainty. Journal of Financial Economics, 145(2), 642–664. https://doi.org/10.1016/j.jfineco.2021.09.009

Bhandari, K. R., Ranta, M., & Salo, J. (2022). The resource-based view, stakeholder capitalism, ESG, and sustainable competitive advantage: The firm's embeddedness into ecology, society, and governance. Business Strategy and the Environment, 31(4), 1525–1537. https://doi.org/10.1002/bse.2967

Bin-Feng, C., Mirza, S. S., Ahsan, T., & Qureshi, M. A. (2024). How uncertainty can determine corporate ESG performance? Corporate Social Responsibility and Environmental Management, 31(3), 2290–2310. https://doi.org/10.1002/csr.2695

DiMaggio, P. J., & Powell, W. W. (1983). The iron cage revisited: Institutional isomorphism and collective rationality in organizational fields. American Sociological Review, 48(2), 147–160. https://doi.org/10.2307/2095101

Edmans, A. (2023). The end of ESG. Financial Management, 52(1), 3–17. https://doi.org/10.1111/fima.12413

Fu, P., Ren, Y.-S., Tian, Y., Narayan, S. W., & Weber, O. (2024). Reexamining the relationship between ESG and firm performance: Evidence from the role of Buddhism. Borsa Istanbul Review, 24(1), 47–60. https://doi.org/10.1016/j.bir.2023.10.011

Gupta, P. P., Lam, K. C. K., Sami, H., & Zhou, H. (2022). Do religion and politics impact corporate governance diversity policy? Asian Review of Accounting, 30(1), 1–30. https://doi.org/10.1108/ara-09-2021-0181

Iamandi, I.-E., Constantin, L.-G., Munteanu, S. M., & Cernat-Gruici, B. (2019). Mapping the ESG Behavior of European Companies. A Holistic Kohonen Approach. Sustainability, 11(12), 3276.https://doi.org/10.3390/su1112327

Jiang, Y., Klein, T., Ren, Y.-S., & Duong, D. (2024). Global geopolitical risk and corporate ESG performance. Journal of Environmental Management, 370,122481. https://doi.org/10.1016/j.jenvman.2024.122481

Kim, J., & Daniel, S. J. (2016). Religion and corporate governance: Evidence from 32 countries. Asia-Pacific Journal of Financial Studies, 45(2), 281–308. https://doi.org/10.1111/ajfs.12127

Kraeussl, R., Oladiran, T., & Stefanova, D. (2022). A Review on ESG Investing: Investors’ Expectations, Beliefs and Perceptions. SSRN Electronic Journal. https://doi.org/10.2139/ssrn.4123999

Liya, Z., Su, C.-W., Baz, S., & Xue, Z. (2026). Governance and greenwashing in the BRICS: The moderating role of national ESG performance in sustainable finance outcomes. Journal of Innovation and Knowledge, 12, 100893. https://doi.org/10.1016/

j.jik.2025.100893

Martins, H. C. (2022). Competition and ESG practices in emerging markets: Evidence from a difference-in-differences model. Finance Research Letters, 46, 102371. https://doi.org/10.1016/j.frl.2021.102371

Martiny, A., Taglialatela, J., Testa, F., & Iraldo, F. (2024). Determinants of environmental social and governance (ESG) performance: A systematic literature review. Journal of Cleaner Production, 456, 142213. https://doi.org/10.1016/j.jclepro.2024.142213

North, D. C. (1990). Institutions, institutional change and economic performance. Cambridge University Press.

Rohendi, H., Ghozali, I., & Ratmono, D. (2024). Environmental, social, and governance (ESG) disclosure and firm value: the role of competitive advantage as a mediator. Cogent Business and Management, 11(1), 2297446. https://doi.org/10.1080/23311975.2023.2297446

Song, H. (2021). Buddhist approach to corporate sustainability. Business Strategy and the Environment, 30(7), 3040–3052. https://doi.org/10.1002/bse.2787

Speece, M. W. (2019). Sustainable development and Buddhist economics in Thailand. International Journal of Social Economics, 46(5), 704–721. https://doi.org/10.1108/ijse-08-2018-0405

Tan, F., & Dipendra, K. C. (2024). Tensions between materiality assessments and stakeholder engagements in Thai corporate sustainability leaders. Sustainability, 16(17), 7711. https://doi.org/10.3390/su16177711

Terzani, S., & Turzo, T. (2021). Religious social norms and corporate sustainability: The effect of religiosity on environmental, social, and governance disclosure. Corporate Social Responsibility and Environmental Management, 28(1), 485–496.

https://doi.org/10.1002/csr.2063

Tsang, A., Frost, T., & Cao, H. (2023). Environmental, Social, and Governance (ESG) disclosure: A literature review. The British Accounting Review, 55(1), 101149. https://doi.org/10.1016/j.bar.2022.101149

Tsang, A., Wang, Y., Xiang, Y., & Yu, L. (2025). ESG Ratings and Dividend Changes: Evidence From the Initiation of Nonfinancial Agency Coverage. Corporate Governance: An International Review, 33(4), 554–577. https://doi.org/10.1111/corg.12615

Tsendsuren, C., Yadav, P. L., Kim, S., & Han, S. (2021). The effects of managerial competency and local religiosity on corporate environmental responsibility. Sustainability, 13(11), 5857. https://doi.org/10.3390/su13115857

Downloads

Published

How to Cite

Issue

Section

License

Copyright (c) 2026 Journal of Contemporary Buddhist Society = JCBS

This work is licensed under a Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License.